California has officially raised the stakes for corporate climate accountability. With the release of new guidance in July and August 2025, the California Air Resources Board (CARB) has clarified the reporting requirements for SB 253 (Climate Corporate Data Accountability Act) and SB 261 (Climate-Related Financial Risk Disclosure)—two landmark regulations that will impact thousands of companies doing business in the states. These updates have wide-reaching implications for ESG, sustainability, legal, finance and risk teams across the U.S., signaling that climate reporting is shifting from voluntary best practice to a core business expectation.

The guidance provides a detailed roadmap for the first reporting cycle, which begins in 2026.

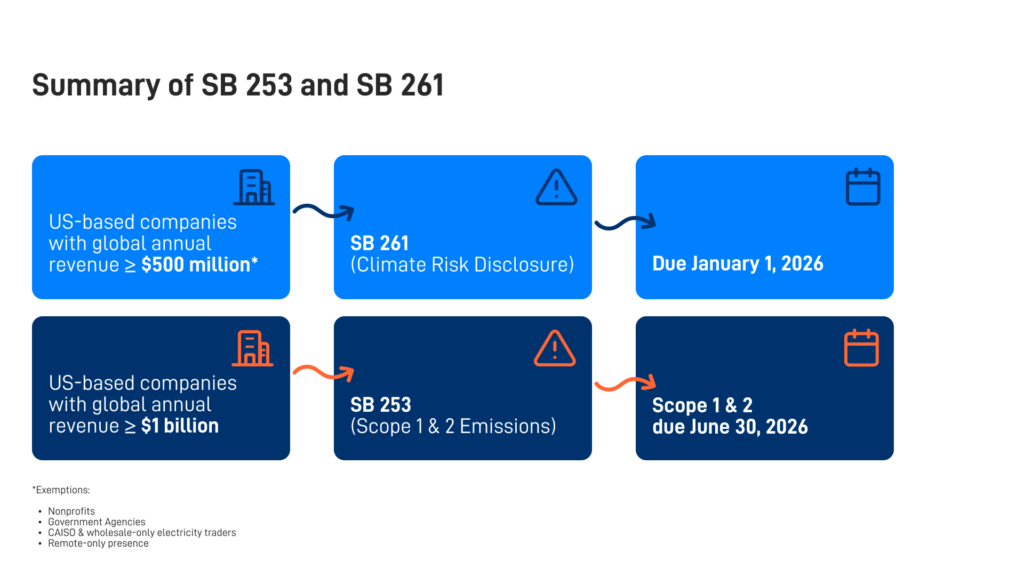

Under SB 253, companies meeting the revenue threshold of $1 billion or more and conducting business in California will need to disclose Scope 1 and Scope 2 greenhouse gas (GHG) emissions for the 2025 calendar year by June 30, 2026. These disclosures will require limited third-party assurance, marking a significant step up from internally validated inventories. CARB plans to publish draft reporting templates in September 2025, giving companies a short runway to prepare robust emissions reporting systems.

SB 261 applies to entities with $500 million or more in annual revenue, requiring them to publish a climate-related financial risk disclosure report by January 1, 2026. These reports must be accessible both on the company’s public website and in CARB’s new online docket, which opens December 1, 2025, and closes July 1, 2026. Importantly, this submission window should not be seen as a grace period; organizations are expected to have their reports ready for publication on day one.

CARB has also shed light on the process of identifying covered entities. The agency will leverage a mix of official state data and commercial sources, such as Dun & Bradstreet and S&P, to compile a preliminary list of companies in Q4 2025. However, the responsibility to self-assess coverage ultimately falls on each organization. Certain exemptions are in place, including nonprofits, government agencies, CAISO and wholesale-only electricity traders and businesses whose only California presence is through remote employees. Investment funds are pushing for broader exemptions, but no final decisions have been made.

Another key update relates to data years. For the first reporting cycle, companies filing under SB 261 may choose to use either 2023–2024 or 2024–2025 data, provided they clearly disclose any limitations. SB 253 reporters, on the other hand, must calculate and report emissions for the full 2025 calendar year. CARB strongly recommends that organizations begin preparing their emissions inventories immediately to avoid last-minute challenges.

Perhaps the most striking message from CARB’s recent workshops is the emphasis on authenticity. Regulators made it clear that these disclosures are not meant to be box-ticking exercises or generic reports generated with minimal effort. The expectation is that organizations will demonstrate real governance structures, internal processes and risk assessments, even if disclosures are qualitative or incomplete in the first year. In CARB’s words: “You can’t just ChatGPT it.”

Finally, CARB has confirmed the implementation of annual flat fees to fund these programs: $3,106 for SB 253 reporters and $1,403 for SB 261 reporters, with adjustments for inflation over time. Organizations subject to both regulations will owe both fees.

To guide organizations in structuring their reports, CARB has confirmed that disclosures must align with recognized frameworks such as the Task Force on Climate-Related Financial Disclosures (TCFD) or ISSB/IFRS S2 standards. Companies that cannot meet every requirement in year one must include clear roadmaps for how they will achieve full compliance over time. While scenario analysis is not mandatory in the first cycle, CARB strongly encourages its inclusion, and qualitative climate risk assessments are acceptable for now—though companies should work toward quantifying risk as they mature their processes.

In terms of assurance, SB 253 introduces escalating requirements, starting with limited assurance in 2026 and moving to reasonable assurance by 2030. CARB has signaled alignment with globally recognized assurance standards, including ISSA 5000, AA1000, ISO 14060 and AICPA frameworks. Companies subject to these rules should start conversations with accredited third-party assurance providers early to ensure capacity.

The overarching message is clear: this is a pivotal moment for climate accountability, and companies should treat it with urgency. Organizations that begin work now—verifying whether they are covered, designating reporting leads, selecting disclosure frameworks, engaging assurance partners and initiating emissions calculations—will be well-positioned to comply with California’s regulations and stay ahead of evolving federal and global standards, including the SEC’s proposed climate rules and the EU’s CSRD.

With draft reporting templates and additional CARB guidance coming in September 2025, there is still time to act. But for sustainability and ESG leaders, the clock is ticking. By embedding climate reporting into governance and risk management processes today, companies can transform these regulatory obligations into opportunities for leadership and transparency.

For deeper insights into SB 253, SB 261 or how these rules intersect with other frameworks, visit the CARB Program Page or connect with our advisory team. We’re here to help you navigate compliance from strategy to execution and ensure your climate disclosures not only meet California’s requirements but also strengthen your global ESG strategy.

Share

Want to learn more?